First Quarter Analysis- Geopolitics and Oil

The first quarter of 2026 illustrates the importance of preparation when it comes to financial planning and investing. After strong gains in 2025, markets have faced a combination of geopolitical shocks, higher oil prices, and renewed economic uncertainty. The conflict in Iran, which began at the end of February, became the dominant market story, pushing oil prices sharply higher and sparking the first market pullback of the year. However, by the end of March, headlines around a possible ceasefire emerged, and the situation continues to evolve.

Taking a broader perspective, markets have still performed exceptionally well over the past twelve months. Beneath the surface, many parts of the market have supported portfolios, including energy and defensive sectors. There will undoubtedly be new market questions in the coming months, including a change in leadership at the Federal Reserve and the midterm election later this year.

For long-term investors, the first quarter is a reminder that markets rarely move in a straight line, and that the principles of sound investing matter most when uncertainty is at its peak.

Key Market and Economic Drivers

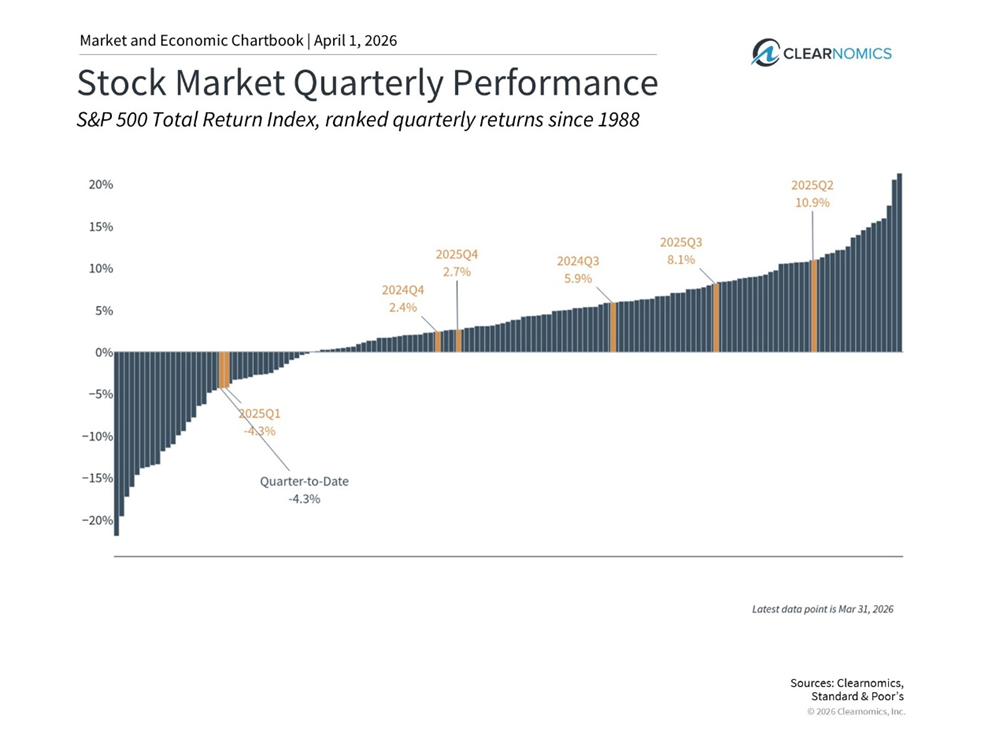

- The S&P 500 experienced a total return of -4.3% in Q1, the Nasdaq -7.0%, and the Dow Jones Industrial Average -3.2%.

- The Bloomberg U.S. Aggregate Bond Index was flat for the first quarter of 2026. The 10-year Treasury yield ended the quarter at 4.3% after falling as low as 3.9% at the end of February.

- Developed market international stocks (MSCI EAFE) were down -1.1% and emerging market stocks (MSCI EM) declined -0.1% over the quarter, both on a total return basis in U.S. dollar terms.

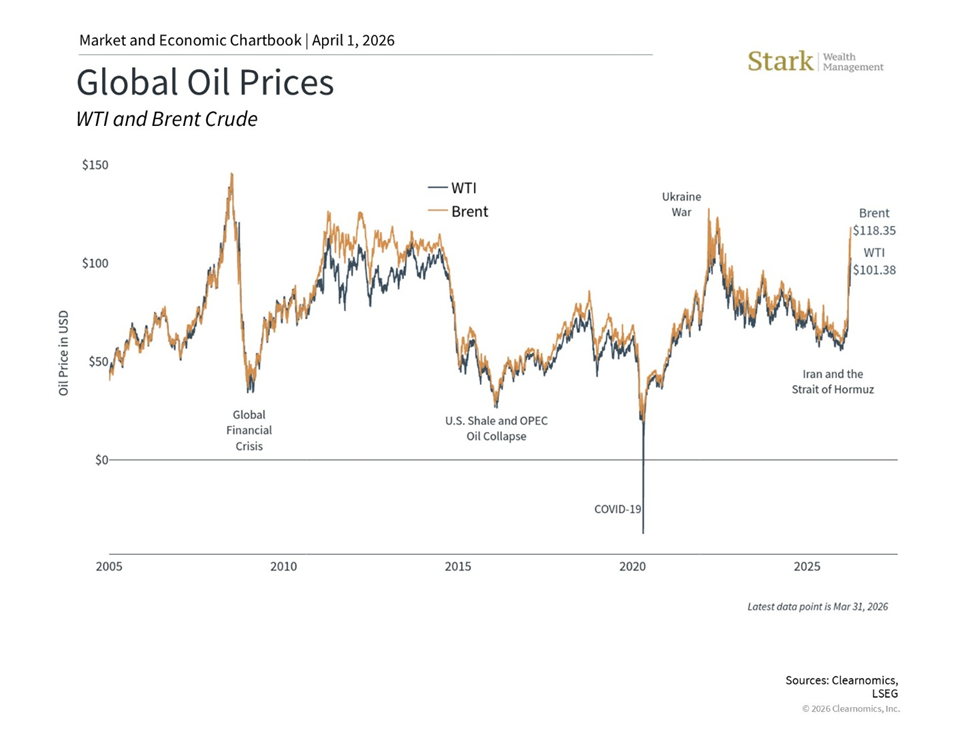

- Oil prices spiked with Brent crude reaching $118 per barrel at the end of March after beginning the year under $61. WTI ended the quarter at $101 per barrel.

- Gold ended the quarter at $4,668 per ounce after climbing as high as $5,417 in January. The U.S. Dollar Index (DXY) strengthened slightly to 99.96 over the same period.

- February inflation showed headline CPI rising 2.4% year-over-year and core CPI climbing 2.5%. The core PCE price index, the Fed's preferred measure, rose 3.1% year-over-year in January.

- The Federal Reserve kept rates unchanged within a range of 3.50% to 3.75% at both meetings during the first quarter.

Markets experienced the first pullback of the year

It’s natural to draw parallels between the start of this year and the beginning of 2025, since both were driven by global concerns. Coincidentally, both first quarter periods experienced pullbacks for the S&P 500 of 4.3%. While last year’s volatility was the result of tariffs and this year’s is due to the conflict in the Middle East, the effect on investor sentiment has been similar. When uncertainty rises, it’s natural for markets to experience short-term swings in response to headlines.

The past is no guarantee of the future, but zooming out can help us understand how markets have behaved historically. Despite the challenges in the first quarter of 2025, the stock market experienced strong gains through the remainder of the year, including dozens of record highs across major indices. The point is not that markets always recover quickly, but that market conversations tend to focus only on negative news. So, when rebounds do occur, they often do so when investors least expect them.

Perhaps the most helpful perspective is to remember that pullbacks are a normal and unavoidable part of investing. Since 1980, the S&P 500 has experienced an average intra-year drawdown of around 15%, even though markets tend to experience positive returns in more than two-thirds of years. It’s natural for the average year to experience four or five pullbacks of five percent or worse. Last year saw six such pullbacks, even though the S&P 500 finished the year with an 18% total return.

For investors, the key takeaway is that short-term market swings, especially those driven by headline risk, are simply part of the market cycle. Portfolios aligned with long-term financial goals are designed exactly to navigate these periods. This could be especially important as we approach the midterm election and fiscal concerns reemerge later in the year.

Geopolitics and oil prices are the primary source of uncertainty

The most significant market development of the first quarter was the escalating conflict in the Middle East, which drove oil prices higher. Disruptions to the Strait of Hormuz, which carries roughly 20% of global oil from the Persian Gulf to the rest of the world, led to production cuts across major oil-producing nations in the region. Brent crude ended the quarter at $118 per barrel, up over 94% year-to-date, while WTI crude surpassed $100, the highest levels since the war in Ukraine began in 2022. Oil will continue to react to geopolitical headlines, including around a possible ceasefire.

Higher fuel costs directly affect consumers through the price of gasoline at the pump and indirectly raise the prices of goods and services across the economy. The average price of gasoline across the country reached $4 at the end of March, and diesel prices have jumped significantly as well.

While these types of events do affect consumer pocketbooks, economists tend to view these types of “supply-side shocks” as temporary when considering the health of the overall economy. This is because oil prices tend to improve once the geopolitical event has stabilized. This was the case in 2022 when gas prices reached $5 before declining within months. While not pleasant, significant financial hardship is not expected to be an issue for the average American household at current gasoline levels.

History also shows that geopolitical events, while creating short-term instability, have not typically derailed markets in the long run. This includes the U.S. operation in Venezuela in January, which surprised markets but had little lasting impact on investments. While the current situation is still evolving and the humanitarian consequences are significant, investors who made dramatic portfolio adjustments in response to past events often did so at the wrong moment.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.