May Market Recap

Market resiliency was on full display this May, even despite heightened uncertainty bubbling under the surface. Equities advanced across the board, supported by continued enthusiasm around artificial intelligence (AI) and better-than-expected corporate earnings reports. The final month of spring also saw a transition in Federal Reserve leadership, rising inflation, and escalating geopolitical tensions—most notably in the Middle East and between the US and China. Taking a closer look at Fed leadership, shifting monetary policy, and inflation trends helps us identify what’s driving equity outperformance against this complex backdrop.

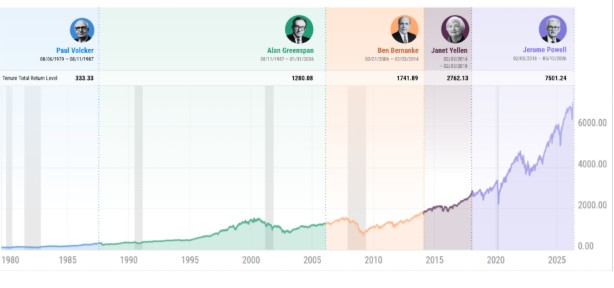

On May 15th, 2026, Kevin Warsh was sworn in as the 17th Chair in the Federal Reserve's 113-year history, marking the end of Jerome Powell’s eight-year tenure. Warsh steps in with the Federal Funds Rate at 3.75%. Markets forecast a more than 50% chance that this remains unchanged through the end of 2026, a projection which reflects uncertainty around Warsh’s policy direction, compounded by rising inflation and the highest level of internal FOMC dissent since 1992. He will inherit a divided committee navigating an increasingly unsettled economic backdrop, but we don’t see these challenges as insurmountable.

Examining the tenure of the last five Fed chairs, we find that each inherited an economy with its own unique set of challenges, yet long-term market performance remained broadly positive, with the S&P 500 returning 3,840% since 1979. Just this May, the S&P rose 5.3%, bolstered by momentum carrying over from April, the best month for the stock index since November 2020.

May gains weren’t restricted to the S&P 500. Across the board, all major market indices posted returns of more than 2.9% last month. Emerging markets topped the charts, gaining 9.7%, while performance on a sector-by-sector basis was less straightforward. The Technology sector led by a wide margin, up 20% for the second month in a row, while the second-best performing sector, Health Care, gained less than 4%. Other sectors landed in the red, including Energy, down 5.6% and lagging for the second consecutive month as the US and Iran work towards a peace solution.

Turning our attention back to the Fed, the US inflation rate increased by 0.5% month-over-month to 3.8%, the highest reading since May 2023. Core inflation (excluding food and energy) increased by a more modest 0.2% month-over-month to 2.8%. We expect this to be a primary topic at the next Fed meeting, scheduled for June 17th.

Investors are currently in the midst of a market defined by tension and uncertainty. The scale of AI-related spending underscores a multi-year transformation that should continue to support productivity, earnings growth, and market leadership within select sectors. At the same time, high levels of AI-related capital investment have started to pressure free cash flow and lend credence to questions about timing and returns, particularly if economic conditions tighten.

We are watching closely as these changing crosscurrents continue to shape the investment landscape, and our core belief is still that strong market fundamentals and a good growth outlook outweigh the current headwinds. Above all, our firm remains dedicated to guiding you through these evolving conditions, proactively adjusting portfolios in alignment with investment objectives, and partnering with you to pursue your long-term goals.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries